Insights

T+1 securities settlement cycle

Share this article

Does a shorter security settlement cycle mean more foreign exchange risk?

Same-day security settlement is moving closer to reality with the decision by the US Securities and Exchange Commission to require security transactions to settle one day after trading, beginning May 28, 2024. The SEC expects the shorter settlement period to reduce risk, cut costs, and modernize securities trading infrastructure. The change will present processing and technological challenges, including those related to currency transactions by foreign investors who need US dollars for securities purchases. Is the FX market ready?

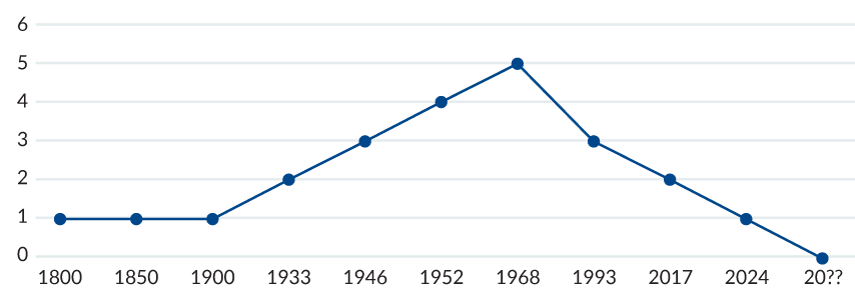

FIGURE 1: US SECURITIES SETTLEMENT CYCLE (DAYS)

Source: archive.org/details/friendsoffinanci00muse_12/page/22/mode/1up?view=theater

Buying or selling securities involves two parts, trading and settlement. Trading determines details of the transaction: the security, quantity, price, and date when the securities and payment will be exchanged (settlement date). In most markets, that settlement date is two business days after trading (commonly described as T+2). The time between trading and the exchange of securities for cash is the settlement cycle. The United States and Canada (which is proposing to align its settlement cycle with that of the United States) will join India and China as the only nations with a T+1 settlement cycle while other markets consider shortening their settlement cycles to harmonize with the T+1 nations.

Changes in security settlement affect FX trading

Cutting the settlement cycle by half affects the time allotted to security processing which, in turn, affects currency trading for foreign investors. As an example, a European investor would need to convert euros to US dollars to buy equities on a US exchange. Often, that currency order is issued after certain security processes, such as allocation and confirmation, are completed.

Foreign exchange (FX) transactions typically have a T+2 settlement cycle and often settle via Continuous Linked Settlement (CLS), the international payment application for settling foreign exchange transactions. Launched in 2002, CLS is a payment versus payment (PvP) system, meaning a transaction is settled only if CLS has received both payments from the two trading parties. If one party fails to deliver its currency, CLS returns the other party’s payment. Because of that PvP benefit, many market participants view CLS as a key component in managing settlement risk, the risk that one party to a foreign exchange transaction won’t deliver the currency it sold.

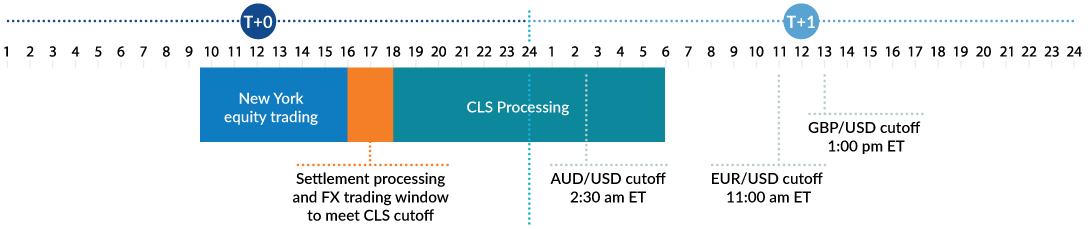

Figure 2 below shows the timeline for the close of equity trading (one type of security affected by the shorter settlement cycle) in New York, CLS processing, and some currency cutoff times to ensure T+1 security settlement.

FIGURE 2: CUTOFF TIMES FOR FX TRANSACTIONS TO SUPPORT T+1 SECURITY SETTLEMENT - EASTERN TIME

Source: Barclays, Commerzbank, Commonwealth Bank of Australia

When the United States moves to T+1 settlement, only two hours will exist to submit FX trade details for CLS processing after equity trading closes. Equity managers and the currency trading entity will need near-flawless processing to meet the CLS deadline. It is likely that issues with some equity or FX trades will arise requiring intervention and manual processing, and the CLS cutoff deadline will be missed.

Even without the CLS deadline there is not much time to process equity transactions, deal with exceptions, and trade foreign exchange to ensure dollars are available for T+1 security settlement. Further complications result from time zone differences. The US equity market closes at 4 pm Eastern Time, 9 and 10 pm in the United Kingdom and Europe. Because of the loss of a settlement day, European securities teams may have to expand processing hours into the late evening or early morning to cover North American trading. Asia is under even more pressure because those nations are one day ahead of the US, resulting in tight currency cut-off times.

Foreign investment managers may consider placing FX trading and settlement teams in North America, although that can be a lengthy and difficult effort. Other options include trading FX to maintain a US dollar cash balance to fund security purchases. This cash might result in a poor return compared to investments in other assets; that underperformance could be overcome with a futures overlay. Futures trading has its own set of challenges including a need for futures expertise and trading and settlement infrastructure.

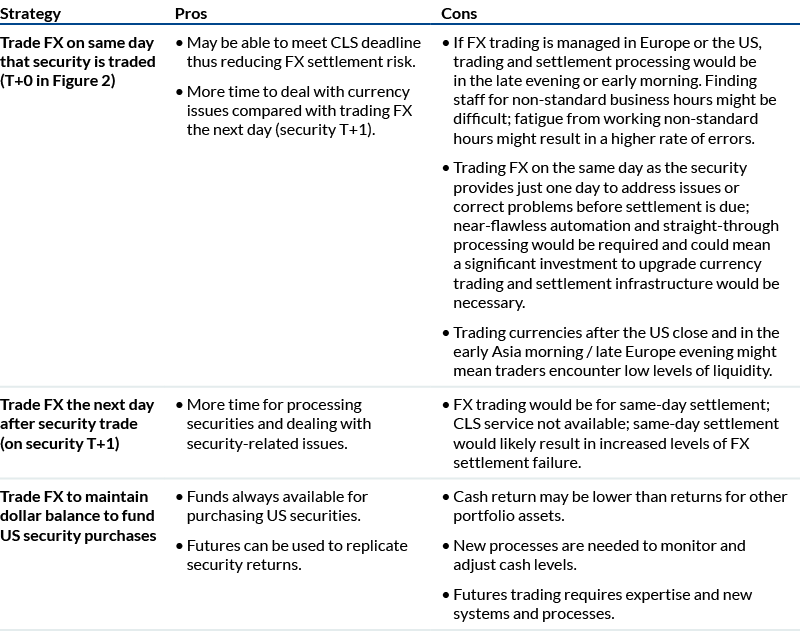

Ways FX trading can support T + 1 settlement cycle

Table 1 summarizes the pros and cons of various FX strategies related to T+1 settlement.

TABLE 1: FX STRATEGIES FOR T+1 SECURITY SETTLEMENT

Shorter security settlement cycles result in significant benefits, ones that would also be advantageous for foreign exchange trading, and the move to T+1 security settlement might be the event that spurs the currency market to upgrade infrastructure and processes to shorten the FX settlement cycle. The key is developing payment versus payment processes to manage the FX settlement risk.

Explore

Central Bank Digital Currencies

What do CBDCs mean for the US dollar as the world's major reserve currency?

US dollar: Currency dynasty

Is the USD's position as the world's reserve currency safe, or is its decline inevitable?

Spark

Our quarterly email featuring insights on markets, sectors and investing in what matters